Health Insurance for Foreign Professionals in Singapore: What You Must Know Before Moving

INSURANCE

Singapore’s healthcare is world-class — but it comes with a price. Unlike Singapore Citizens and Permanent Residents, foreign professionals are not covered under MediShield Life, the national health insurance scheme.

This means your protection depends entirely on employer coverage and any private health insurance you secure yourself. Without the right plan, even a short hospital stay could result in significant out-of-pocket expenses.

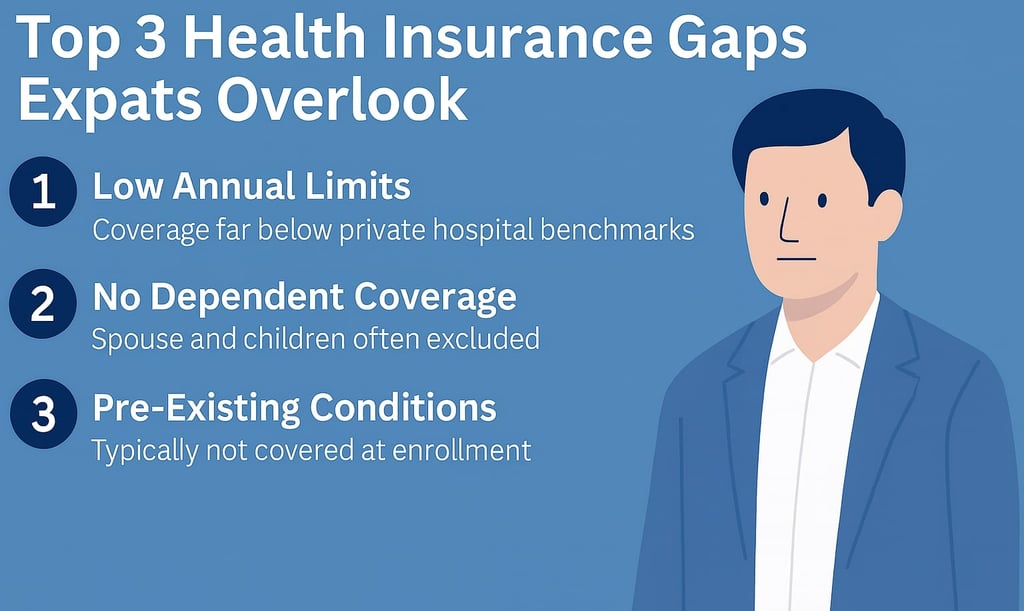

1. Why You Can’t Rely on Employer Coverage Alone

Most employers in Singapore provide some form of medical benefit, but it is usually basic:

Low annual limits compared to MOH’s fee benchmarks for private hospital procedures.

Dependents often excluded — spouse and children may not be covered.

Pre-existing conditions generally not covered, unless explicitly included.

Coverage ends when you leave or change employers, leaving you unprotected.

💡 Action: Ask HR for the plan’s benefit summary. Compare annual limits against MOH benchmarks to check if they would realistically cover private hospital care.

2. Key Coverage Areas Expats Should Prioritise

When choosing a plan in Singapore, look beyond the basics:

Inpatient & Emergency Care – Hospitalisation, surgery, and A&E.

Specialist & Outpatient Care – Diagnostic scans and follow-ups.

Pre-Existing Conditions – Typically excluded, but some plans or riders may offer limited cover.

Family Coverage – Ensure your spouse and children are protected.

Portability – Look for plans that remain valid if you change jobs or relocate.

3. The Biggest Pitfalls Expats Face

Assuming employer coverage is enough – until a claim shows otherwise.

Buying insurance too late – once a health issue arises, it is usually excluded.

Ignoring exclusions – high-risk sports, maternity, or mental health may not be covered.

💡 Action: Always review the “Exclusions” section in detail, not just the highlights.

4. Smart Strategies for Expats in Singapore

Top Up Employer Coverage – Use personal plans to close gaps.

Annual Multi-Trip Plans – Combine health and travel protection if you travel frequently.

Budget for Family Needs – Add maternity, dental, or child health benefits if relevant.

Review Annually – As your career and family evolve, so will your insurance needs.

Final Thoughts

For foreign professionals, health insurance in Singapore is not optional. Without MediShield Life, you must actively secure the right coverage to avoid financial risk.

Understanding what’s excluded, checking your employer plan against MOH benchmarks, and adding the right top-ups will give you peace of mind and financial security.

💡 Next Step: If you’d like a review of your current health insurance plan, I can help identify gaps and recommend tailored solutions suited for expats in Singapore.